Welcome to the world's largest alternative investing newsletter! Join 90,000 others and see what you've been missing.

☢️ Uranium Investing

|

Welcome to the Alts Sunday Edition. Hope you enjoyed last week's issue on Opportunity Zones. Few investment opportunities are as controversial as the element uranium.

In the wrong hands, uranium is capable of powering the most devastating weapons humanity has ever devised. But in the right hands, uranium could power a future with unlimited, reliable, low-carbon energy. While nuclear power has flaws, policymakers have become increasingly interested in nuclear to make up for shortfalls in renewable energy without turning to fossil fuels. That trend has translated into increased demand for uranium, resulting in soaring prices for the element and healthy profits for some uranium investors. Today, we’re breaking down the uranium trade, exploring the opportunities and challenges that investors may face. The first half of this issue is free:

You'll need the All-Access Pass to unlock the second half 🔒

Along the way, you'll also learn a ton about nuclear power, including some of the biggest misconceptions about this energy source (and why its future might actually be uranium-free.) Let’s go 👇

A short primer on the Uranium lifecycleTo understand the uranium market, you need a basic understanding of the element itself – including how it’s produced, refined, and enriched. Despite a reputation for elusiveness and rarity, uranium is a surprisingly abundant element. In its raw form, uranium is about as common in the earth’s crust as tin or zinc (you can literally buy uranium ore on Amazon!) But as you might expect, environmental concerns make mining uranium slightly more complicated than mining other elements. How uranium is minedClassic open-pit or underground shaft mining are common ways of extracting uranium from the earth. But here’s the thing – while a lone piece of uranium ore isn’t very dangerous (you can even handle it with your bare hands) the buildup of large amounts of uranium ore can pose a radiological problem.

Therefore, modern approaches usually involve in-situ leaching, where miners pump a liquid solution into the ground to dissolve uranium and then pump the now-uranium-filled solution back out. This video (1:44) shows how the in-situ leaching process is used to extract uranium. Whatever approach you use, there’s no avoiding the massive investment of both time and money it takes to start a uranium mine. Equipment for new mines can cost more than $100 million. Meanwhile, the lag time before the mine can start producing ore stretches from 10 to 15 years. Once the ore is out of the ground, uranium’s next step is refinement and enrichment. Enriched uranium: A matter of degreeAfter uranium is mined, it’s separated and dried into a refined form – commonly known as yellowcake.

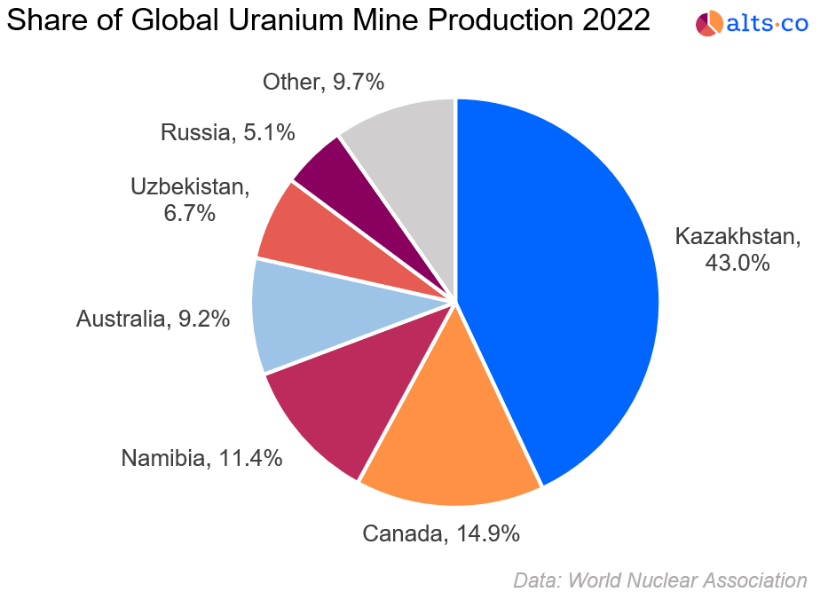

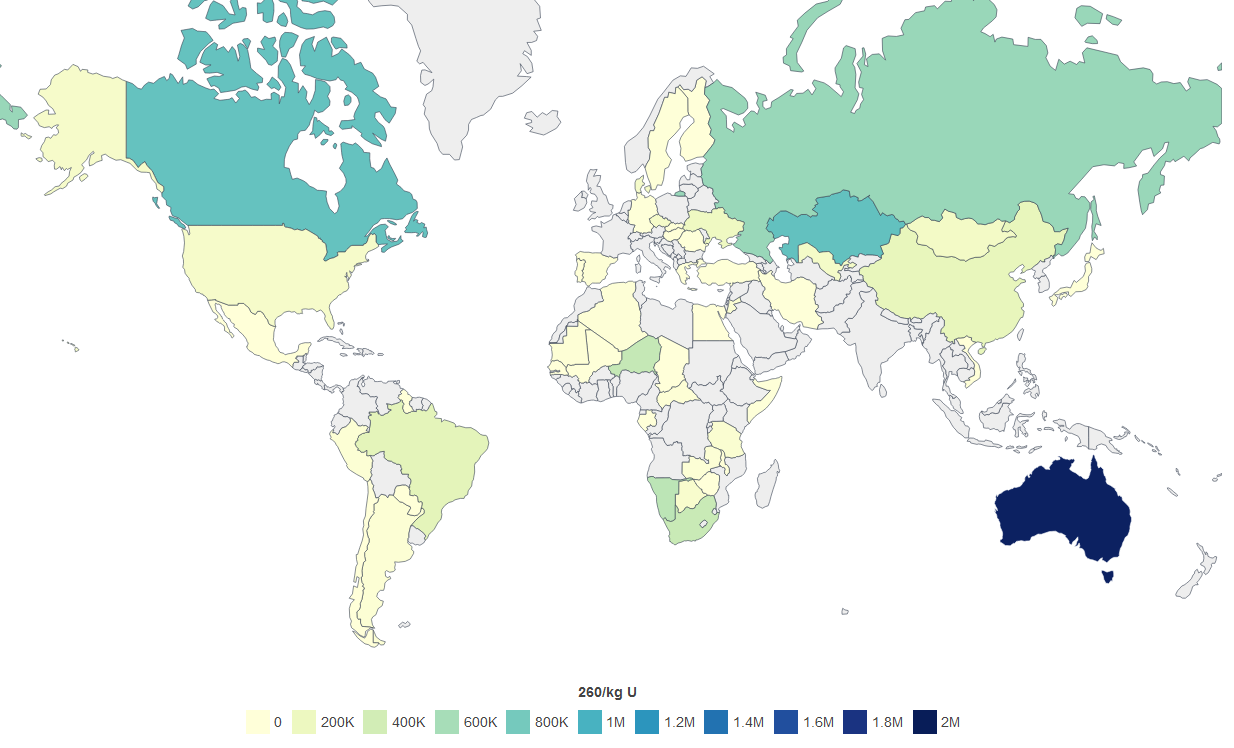

Next, yellowcake is converted into a gaseous state and fed into centrifuges, which spin the gas rapidly. These centrifuges separate the uranium isotopes in the gas to increase the proportion of the highly reactive uranium-235 in the gas – a process known as enrichment. The level of enrichment achieved dictates whether the uranium is useful as nuclear fuel or in a nuclear bomb. Reactor-grade uranium is 3-5% enriched, while weapons-grade is more than 85% enriched – big difference! In other words, the exact same process that creates reactor-grade material can also create weapons-grade material – it’s simply a matter of degree. The state of Uranium supplyI mentioned that uranium is quite an abundant element. While that’s true, it’s only true on average. Very few countries have been blessed with sizable stockpiles of uranium. In fact, global supply of the element is mostly concentrated in just a few regions of the world. Where is the uranium?Just three countries have more than 50% of the world’s proven uranium reserves: Australia (28%), Kazakhstan (13%), and Canada (10%). But this data doesn’t tell the full story. The location of uranium reserves is closely tied to uranium production – but it’s not 1-to-1. In Australia, for instance, the uranium mining industry has been a matter of intense debate for years, both on environmental and ethical grounds – meaning production levels lag reserve levels. Despite placing 2nd in uranium reserves, Kazakhstan is by far the world leader in uranium production, producing 43% of the world’s mined uranium in 2022. Canada and Namibia take 2nd and 3rd in global production, with China being a huge investor in Namibia’s recent uranium development.

But as it turns out, a sizable minority of uranium supply doesn’t even come from mines… The uranium recycling industryMines are the primary source of uranium – but there’s also a diverse array of secondary sources that provide either recycled or repurposed uranium for use:

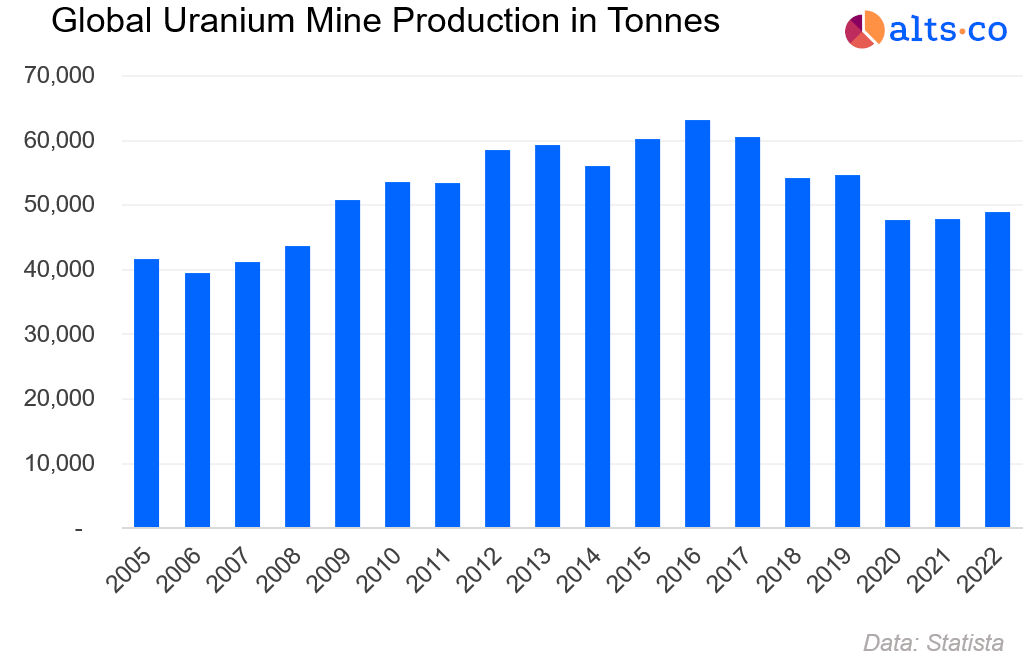

In 2013, secondary uranium sources satisfied just 9% of global demand. But by 2022, that figure had risen to 26%. Increased reliance on secondary sources highlights how primary production struggles to catch up to rising global demand. Why is Uranium supply struggling to match demand?Today, there are 437 operational nuclear plants worldwide, which provide about 10% of global electricity. And all these plants need uranium to fuel them, with global demand currently hovering around 70,000 tonnes per year (about twice the annual demand for silver).

That demand looks set to increase markedly. Globally, about 60 new reactors are already being built with another 110 planned. But at the moment, supply is poorly equipped to meet growing demand – for a few reasons:

While soaring uranium prices caused by these supply struggles should encourage more primary production investment, this isn’t a problem that can be solved overnight. Enrichment bottlenecks compound supply challengesWhile the uranium supply crunch is mostly about primary and secondary capacity, bottlenecks in the enrichment process also pose a threat. Unsurprisingly, governments monitor enrichment technology closely, meaning only a few companies are licensed to operate in this space.

Urenco is owned in 3 parts by the UK and Dutch governments and German utility companies and controls about 25% of global enrichment capacity (including facilities in all 3 countries).

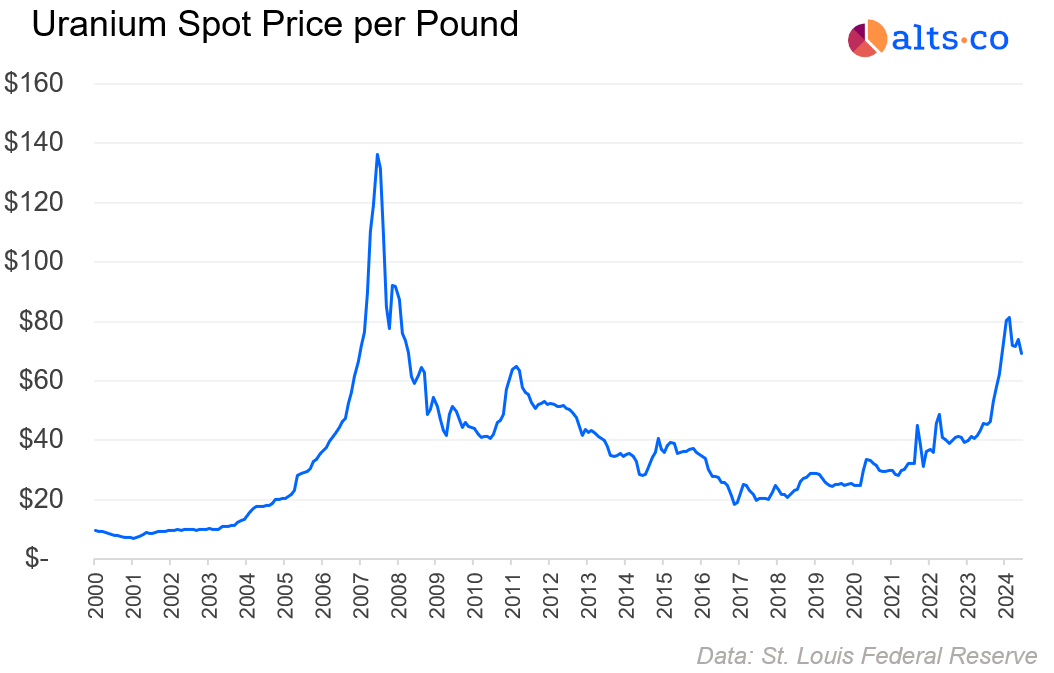

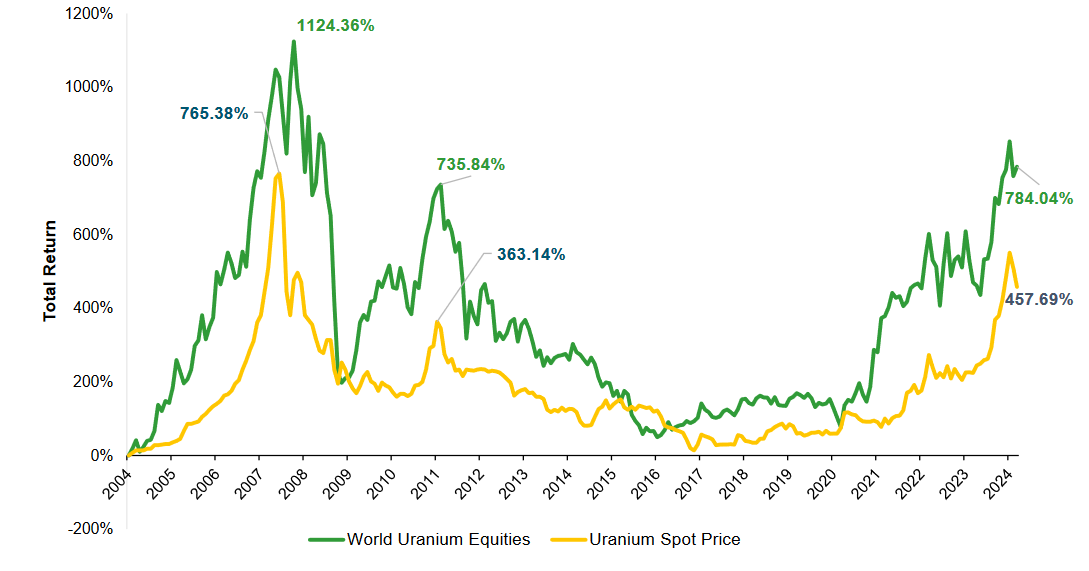

While scaling up enrichment capacity can be done quicker than building reactors or new mines, it’s still a multi-year process that requires significant capital investment. The Uranium bull caseUranium prices have seen a surprising resurgence over the past few years. After the pop of uranium’s pre-GFC bull run, the Fukushima disaster in 2011 seemed like the final nail in the nuclear coffin, set to squash uranium demand permanently. But after about five years in the doldrums, prices gradually started to climb again around 2017, hitting pre-Fukushima levels of up to $80/pound in 2024.

This latest bull run has renewed investor interest in the element, with some speculators betting on the start of a fresh uranium supercycle. Here are the best arguments for being bullish on uranium in the near term... Nuclear power’s unique traits will result in increased adoptionThe basic ideas behind nuclear power are surprisingly simple:

This video (4:50) explains how a nuclear reactor works with a bit more depth. In the context of the global energy transition away from fossil fuels, this process occupies a unique niche:

While nuclear power costs are almost certainly higher than renewables and many fossil fuels, part of this priciness stems from the “soft costs” associated with building a plant, including red tape and regulation – which can be streamlined with enough political will. Finally, nuclear is starting to shed its reputation as a particularly dangerous energy source. When compared on an equivalent basis, nuclear is one of the safest forms of energy – although the salience of events like Chernobyl or Fukushima usually makes us think otherwise. And the example of countries like France, where nuclear now provides nearly 70% of electricity without any major historical accidents, provides increased evidence that nuclear power can be offered safely.

As reactor technology improves (including the growing potential of small modular reactors), safety concerns should continue to alleviate. Uranium supply will not be able to keep up with demandThe world needs uranium to realize the benefits of nuclear power, but the argument is that there just won’t be enough. I’ve already discussed the material reasons why uranium supply might lag, including long lead times and huge costs for new mines. But geopolitical supply disruptions are arguably even more pressing. Kazakhstan is the biggest player in uranium production, and it’s a landlocked country sandwiched directly between China and Russia. Both Vladimir Putin and Xi Jinping have been cozying up to Kazakhstan’s president Kassym-Jomart Tokayev, signing numerous energy-related deals.

Russia already controls almost a quarter of Kazakhstan's uranium production, and Chinese companies now have agreements entitling them to about 60% of the country’s future uranium production. The US, meanwhile, has already taken steps to aggravate Russia over the element, banning all imports of Russian uranium in May (these imports previously accounted for about 12% of domestic supply). You don’t have to be a policy analyst to think that it’s only a matter of time before China and Russia put the screws to Kazakhstan, “encouraging” the country to halt uranium exports to Europe and the US (who rely on Kazakhstan for 23% and 25% of uranium imports, respectively). And considering that the authoritarian ruling party of Kazakhstan seems to owe its grip on power to the Russian military, I’d imagine that encouragement would be pretty convincing. Uranium enrichment, meanwhile, provides just another pressure point for China and Russia to needle the West. Combined, the two countries control more than 50% of global enrichment capacity. The idea that uranium supply chains might completely fracture in the next decade isn’t unreasonable, with US/Europe/Canada/Australia in one corner and Russia/China/Kazakhstan in another. The end result would be far less uranium available for the West and higher prices. Nuclear power demand isn’t sensitive to uranium pricesThe final component of the bull case is the assertion that nuclear power demand wouldn’t fall due to supply-induced uranium price hikes. If demand for nuclear power dwindles because of higher uranium prices, then there’s a natural “ceiling” on how high prices can go. But although nuclear power can be costly, uranium itself isn’t actually a big part of the expense. Fuel accounts for just 5-10% of the cost of electricity generated from nuclear power, indicating that even higher uranium costs wouldn’t really help. Contrast this with an energy source like coal power, where fuel can amount to more than 50% of the cost. The Uranium bear caseThe bull case for uranium is compelling, especially considering prices have already risen sharply in the past few years. But there’s also a bear case, which consists of a few reasons why the current bull run might rapidly decay. The West could secure its own uranium supplyGeopolitical risks loom large over the uranium supply chain – but if Russia and China cut off Western access to Kazakhstani uranium, the situation is far from hopeless. Canada and Australia are the world’s 2nd and 4th largest producers, respectively, and the two countries control almost 40% of global reserves. Add in supply from countries like Ukraine, South Africa, and Brazil, and it’s clear that there’s plenty of uranium available for the West to access.

Yes, it would take time to rebuild uranium supply chains – but in many places, the process is already underway:

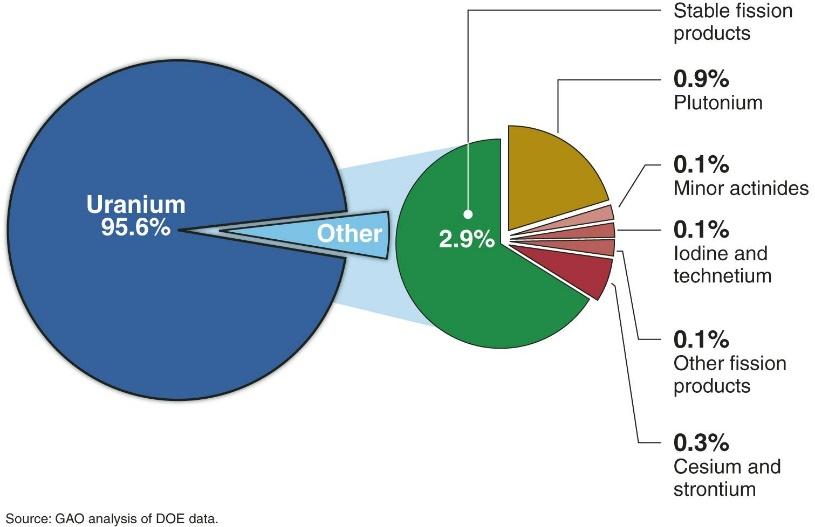

Ultimately, markets wouldn’t be able to avoid the price shock associated with supply chains fracturing – but effectively utilizing the West’s ample uranium resources can help diminish that shock and bring prices under control over the long term. Uranium supply might be price-sensitiveThe bull case argued that uranium demand isn’t very price sensitive, since fuel accounts for a small portion of the cost of nuclear power. But what about uranium supply? Mines in Western countries are expanding not simply due to geopolitical supply threats but directly responding to rising market prices. Even in the US, where the domestic mining industry has dwindled in recent years, at least five mines are being restarted as current prices once again make them economically viable. Potentially even more important than mines, though, is an increased focus on secondary reprocessed uranium. When nuclear fuel comes out of a typical reactor, up to 90% of the potential energy remains, even after up to five years in use. While some countries like France reprocess a substantial amount of nuclear material, doing so hasn’t always been cost-effective, considering the low price of new uranium. But if the uranium supply crunch continues, investments in reprocessing facilities could pay off, dramatically lengthening the life of current uranium stocks (and reducing the burden of nuclear waste to boot).

Nuclear power could become more efficientAs the story of solar power shows, the efficiency of a particular energy source isn’t fixed. Over time, technological improvements usually allow us to wring more energy out of a unit of fuel. While nuclear power’s efficiency gains are nowhere near the level of renewables, there is some track record of improvement here:

As I just described, increased use of reprocessed uranium is one area where uranium efficiency can be improved. But improved reactor technology can also do a lot, including advanced design proposals like the sodium-cooled fast reactor or molten salt reactor. Increased nuclear power efficiency would likely be bad for uranium prices since there will be less demand per reactor (although the increased cost-efficiency of nuclear might raise demand overall). Ultimately, though, the future of nuclear power might not involve uranium at all. Nuclear power could go uranium-freeThroughout this issue, I’ve painted the rising demand for nuclear power as inextricably linked with rising demand for uranium. But what if that’s not the case? It’s possible to build reactors that don’t use uranium a primary element. Thorium, for instance, has long been considered as a potential alternative to uranium. Thorium comes with several benefits, including:

So far, thorium has only been used in a few experimental reactors, including at least one large-scale test in China. And the metal does have drawbacks, like a comparatively higher cost of mining. But thorium isn’t the only route by which nuclear power could go uranium-free. The nuclear fusion process, for instance, uses lighter elements like hydrogen – although a viable fusion reactor prototype seems to be decades away. A high-profile accident could kill nuclearPossibly the greatest threat to nuclear power’s future (and therefore uranium demand) is another major accident. The 2011 Fukushima disaster tanked the uranium market for years and caused many countries to cancel plans for future reactors. While the safety of reactor designs improves with each generation, the threat of an accident that would freeze global enthusiasm for nuclear power lurks in the background.

Investing in UraniumIf you find the bull case for uranium more convincing than the bear case, you can use a few different investment options to ride the trend. Uranium minersUranium mining companies are one way to get exposure to uranium prices since their share prices have historically roughly tracked the spot price of the element.

There are two main classes of miners:

While many junior uranium miners trade on pink sheet markets, some of the larger juniors include:

Sprott offers a junior uranium miner ETF, which includes these and other companies (Nasdaq:URNJ). Publicly accessible senior uranium miners include:

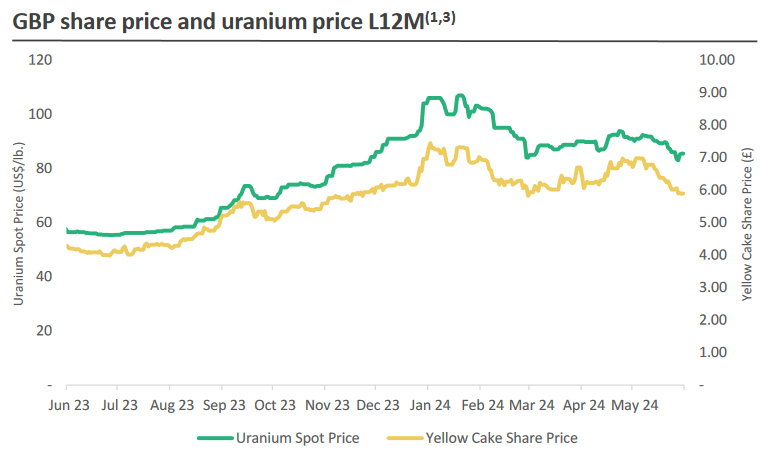

Sprott also offers a broader uranium miners ETF which includes these senior miners, some junior miners, as well as some non-miners and uranium spot positions (NYSE Arca:URNM). VanEck has a similar ETF (NYSE Arca:NLR). Another niche option related to mining is uranium royalty companies. We’ve spoken about mining royalties before in the context of gold, but companies like Uranium Royalty Corp (Nasdaq:UROY) allow investors to access a similar model in this space. Enrichment companiesFurther along the uranium supply chain are enrichment companies, which could be an even more appealing play than miners if supply chains start to fracture. Unfortunately, public uranium enrichment companies are few in number. One option is Centrus Energy Corp (NYSE American:LEU) which recently delivered the first batch of a type of advanced nuclear fuel (high-assay, low-enriched uranium) to the US Dept. of Energy. Another is Silex Systems Ltd (ASX:SLX), an Australian company commercializing a laser-based uranium enrichment technology through their joint-ownership of Global Laser Enrichment. Physical uraniumFinally, investors can consider purchasing physical uranium as the most direct form of exposure to the element’s price. I wouldn’t recommend DIY-ing this investment, but Sprott does offer an exchange-listed uranium trust (TSX:U.U) which custodies more than 65 million pounds of uranium. Another option here is Yellow Cake plc (LSE:YCA), which appears to be structured as a standard company and currently holds about 21 million pounds of uranium.

That's all for today. Reply to this email with comments. We read everything. See you next time, Disclosures

|

Hi! We're Alts.co 👋

Welcome to the world's largest alternative investing newsletter! Join 90,000 others and see what you've been missing.

You are subscribed to The WC Unfollow this topic 📅 January 22, 2025📖 Read time: ± 3 minutes Welcome to the WC, wherein you're trapped in my mind for eight to ten minutes weekly. This week, you've got three revolting/disgusting/delicious stories to digest: 📙 Tracking Trump 🐄 My cow gallstone enterprise seeks investment 🌍 West African booze is big time Let's go. 🚀 CapitalPad: Big returns from small, profitable businesses 🪚 Invest in America's "boring" businesses with CapitalPad As baby boomers...

Read full issue Welcome to the Alts Sunday Edition 👋 Boy, do I have a terrific issue for you today. We just wrapped up a weeklong Investor Trip to Nashville; and I can't wait to tell you about it. This was the music adventure of a lifetime. We arrived eager to understand what's really happening in this complex industry. We returned with industry connections, lifelong friendships, and confidence in an upcoming music investing deal we're cooking up with our friends at JKBX. (More on that below)...

Read online Welcome to the Alts Sunday Edition. Hope you enjoyed last week's issue on our upcoming Investor Trip to Nashville. (It's gonna be epic. Apply here to join.) It's not often that niche tax topics are used to score political points. But in last month's US presidential debate, Donald Trump did exactly this when he bragged about launching opportunity zones. Opportunity zones (OZs) were first implemented as a small but significant part of Trump’s 2017 Tax Cuts and Jobs Act. The idea...